Demand and supply

Supply Curve¶

Determinants of Supply¶

The supply curve illustrates how the quantity supplied responds to changes in various factors. Below is a breakdown of the determinants:

| Determinants | Effect on Curve |

|---|---|

| Price | Move along curve (no shift) |

| Input price | Shift curve |

| Technology | Shift curve |

| Expectations | Shift curve |

| Number of sellers | Shift curve |

Note

When price decreases while income remains constant, consumers' purchasing power increases.

Elasticity Concepts¶

Price Elasticity of Demand (PED)¶

Formula:

PED = \frac{\Delta \text{Quantity Demanded\%}}{\Delta \text{Price\%}} $$ $$ PED \in [0, +\infty)Types of Price Elasticity of Demand¶

-

Perfectly Elastic Demand : The demand curve is a horizontal line.

-

Relatively Elastic Demand

: Percentage change in quantity demanded exceeds percentage change in price (). -

Unit Elastic Demand

: Percentage change in quantity demanded equals percentage change in price (). -

Relatively Inelastic Demand

: Percentage change in quantity demanded is less than percentage change in price (). -

Perfectly Inelastic Demand

: The demand curve is a vertical line.

Total Revenue and Elasticity¶

2.2 Price Elasticity of Supply (PES)¶

Formula:

PES = \frac{\Delta \text{Quantity Supplied\%}}{\Delta \text{Price\%}} $$ $$ PES \in [0, +\infty)Simple Formula¶

Mid-Point Formula¶

Types of Price Elasticity of Supply¶

-

Perfectly Elastic Supply

: The supply curve is a horizontal line. -

Relatively Elastic Supply

: Percentage change in quantity supplied exceeds percentage change in price (). -

Unit Elastic Supply

: Percentage change in quantity supplied equals percentage change in price (). -

Relatively Inelastic Supply

: Percentage change in quantity supplied is less than percentage change in price (). -

Perfectly Inelastic Supply

: The supply curve is a vertical line.

2.3 Income Elasticity of Demand (YED)¶

Formula**: $$ YED = \frac{\Delta \text{Quantity\%}}{\Delta \text{Income\%}} $$

2.4 Cross-Price Elasticity of Demand (XED)¶

Formula:

Market Equilibrium¶

Equilibrium Price¶

The equilibrium price is the point where the Demand Curve and Supply Curve intersect.

Changes in Supply and Demand¶

| No Change in Supply | Increase in Supply | Decrease in Supply | |

|---|---|---|---|

| No Change in Demand | , | , | , |

| Increase in Demand | , | , | , |

| Decrease in Demand | , | , | , |

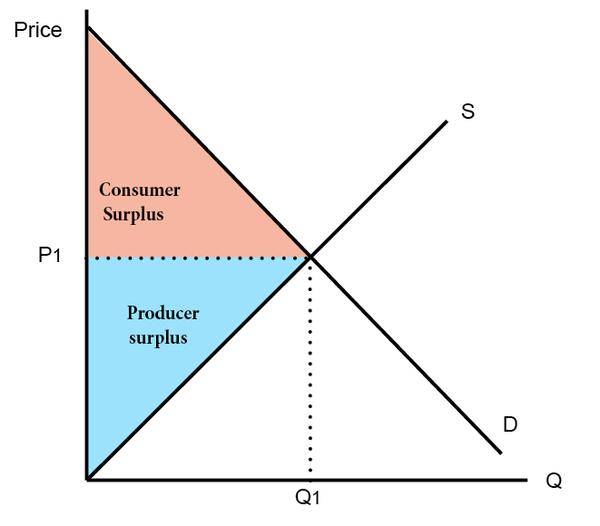

Consumer and Producer Surplus¶

Consumer Surplus¶

- Willingness to Pay (WTP): The maximum price a consumer is willing to pay for a good or service.

- Marginal Buyer: The consumer who leaves the market first if the price rises further.

Producer Surplus¶

- Marginal Seller: The producer who leaves the market first if the price decreases further.

Total Surplus¶

Government Intervention in Markets¶

Price Ceiling¶

- Effective only when actual price > price ceiling.

- Causes a shortage:

$$ \text{Shortage} = QD - QS $$ - Protects consumers.

Price Floor¶

- Effective only when actual price < price floor.

- Causes a surplus:

$$ \text{Surplus} = QS - QD $$ - Protects producers.

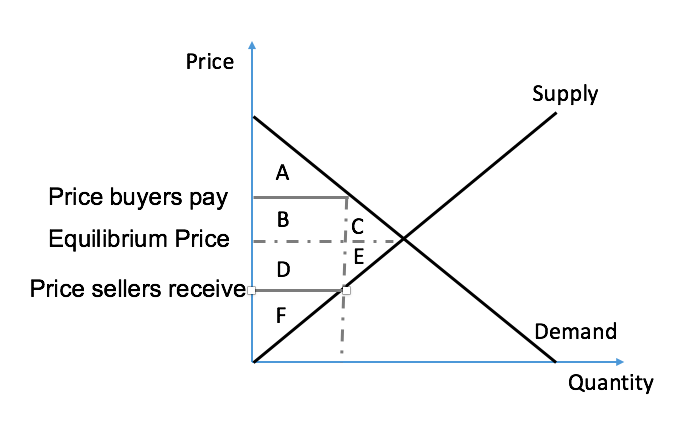

Taxes¶

- Tax burden depends on elasticity:

$$ \text{Inelastic} \implies \text{Higher tax burden} $$ - Size of tax:

$$ \text{Size of Tax} = \text{Price of Demand} - \text{Price of Supply} $$ - Tax revenue:

$$ \text{Tax Revenue} = T \cdot Q $$

Impact of Taxes on Surplus¶

| Without Tax | With Tax | Change | |

|---|---|---|---|

| Consumer Surplus | |||

| Producer Surplus | |||

| Tax Revenue | None | ||

| Total Surplus |